Commercial Aerospace Industry Through COVID-19 Summer 2020 Headwinds

Thousands of layoffs and aircraft removed from service created a whirlwind summer of operational decision-making by commercial aerospace OEMs that will impact the industry for the remainder of this decade.

Thousands of layoffs and aircraft removed from service, combined with a number of major airlines grounding planes and filing for bankruptcy, created a whirlwind summer of operational decision-making by commercial aerospace OEMs that will impact the industry for the remainder of this decade.

In early to mid-April, during the high point of global air travel restrictions and the low point of flight activity, 60 percent of the global in-service fleet of commercial airliners were parked. Operators saw passenger traffic drop by 90 percent worldwide during the second quarter of the year.

At least 25 airlines filed for bankruptcy between April and June, including major Latin American carriers such as LATAM, regional powerhouses like South Africa Airways and prominent U.S. and European carriers such as Air Berlin, Flybe, and Miami Air, among others. The International Air Transportation Association (IATA) projects the commercial airline industry will collectively experience a $90 billion revenue drop for the year.

Most aerospace executives and experts expressed — through second quarter earnings calls, statements and leadership changes — their belief that passenger demand for the commercial airline industry will not return to 2019 levels for at least two to three years. An immediate concern resulting from the overall downturn is the loss of so many commercial aircraft orders and deliveries.

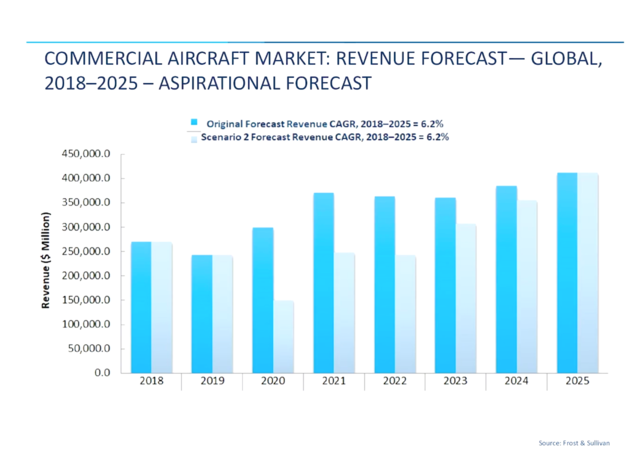

Frost & Sullivan Senior Commercial Aerospace Analyst Timothy Kuder readjusted his firm’s 2018-2025 commercial aircraft revenue outlook based on the impact of COVID-19, projecting astronomical losses based on new orders and deliveries that were supposed to take place.

“That loss that we’re going to have between 2021 and 2023, those deliveries are not ever going to come back,” Kuder said during an opening keynote presentation for the 2020 Global Connected Aircraft Cabin Chats virtual webcast series. “The quantification of that is around $475 billion, and that’s from aircraft production that we thought was going to be there in the next five years. That’s gone and we’re never going to see it again.”

The adjustments to airline schedules and COVID-19’s impact on the financial stability of carriers has had a rippling impact across the commercial side of the aerospace supply chain. With the exception of some regional and cargo operations who had orders in the process, many airlines no longer require the deliveries of any new aircraft as they take existing ones out of service.

Tier 1 and 2 suppliers can survive and find ways to innovate, but if too many key mid and low level components suppliers drop out of the market as a result, they to could start to feel the shock as well, especially in keeping up with production for commercial aircraft and government or defense derivatives that use those same commercial systems and components. Examples include the KC-46A air tanker-refueling configuration of the Boeing 767 airliner or the Airbus A330 Multi Role Tanker Transport (MRTT).

The Center for Disease Control’s (CDC) guidelines for manufacturing facilities include screening employees for COVID-19 symptoms, using physical barriers or modifying workstations to reduce employee contact and increasing frequency of cleaning and disinfection. Following these guidelines has complicated the nuts and bolts of assembling aerostructures and components, said Robin Lineberger, leader for Deloitte’s U.S. and global aerospace and defense divison.

“Assembling the aircraft is challenging in a COVID environment, as companies continue to look at the manufacturing floors, and how they do the assembly, and of course their supply chain beneath them has the same two-fold problems,” Lineberger said. “Slowdown in demand, and then for the demand that they have it is the ability to re-align the facilities where they can produce at those levels,” Lineberger said.

According to Deloitte’s mid-year 2020 aerospace and defense industry outlook report, the global commercial aircraft order backlog collectively stood at 14,100 aircraft. That’s only a marginal drop from the 2019 levels of 14,300; however, “with further cancellations expected and a bleak outlook for new orders in the second half of 2020, the backlog levels are expected to decline,” the report concluded.

“As a result of all of that stress, there is a cash liquidity overhang, and so we fully expect to lose firms at those levels below tier one and tier two,” Lineberger said. “We expect some consolidation there as well, which also complicates another element, which is now whether the components are available to meet the existing demand that we do have if we lose key suppliers.”

The start of the second quarter saw an industry-changing merger of equals between Raytheon and United Technologies that re-aligned Collins Aerospace and Pratt & Whitney under Raytheon Technologies. All companies involved in the merger saw a major impact to the commercial and business jet sides of their business, while defense remained relatively unchanged.

Raytheon’s second quarter earnings report showed commercial OEM sales down 42 percent for Pratt’s largest commercial engine. Aftermarket sales were down 51 percent compared to the second quarter of last year, and “legacy large commercial engine shop visit inductions” were also down 64 percent.

Up and down the supply chain, from suppliers of avionics to fuselages, companies are being forced to shed jobs while continuing to operate at drastically lower levels of production.

Astronics Corp., a large supplier of electronics systems to major commercial aerospace OEMs, had technology advancements in the form of new family of avionics interfaces for “SuperSpeed USB 3.1” unveiled in a July 8 press release and completion of a successful test flight using their antenna to enable LuxStream business jet connectivity. With 70 percent of the company’s business on the commercial side, there is uncertainty ahead for Astronics, although CEO Peter Gundermann told analysts that they’re “well positioned to get through the immediate future.”

“During the quarter, major manufacturers, including primarily Boeing and Airbus, started pulling back on production plans. They have been pulling them back successively as the quarter went on, and even this week a little bit more than we expected,” Gundermann said. “Seventy percent of our traditional market has been involved in commercial transport airplane, and it's been pretty badly affected by the pandemic. Another ten percent traditionally comes from business jet manufacturing. Rates are down there also, maybe not quite as much as commercial transports, but that part of our business is also under stress. The final 20 percent comes from government and defense revenue streams. Demand here has held up reasonably well.”

FLYHT, a Calgary, Alberta-based supplier of flight data acquisition and management systems, made some strategic policy and executive changes in the second quarter. William Tempany was appointed the company’s temporary CEO, taking over for Tom Schmultz who had held the position since October 2015.

The avionics supplier saw a net loss of $277,000 for the second quarter, compared to a net income of $1.03 million during the same period a year ago. In his Aug. 5 letter to shareholders, Tempany said that FLYHT’s current strategic focus is to augment the existing avionics technology it supplies for airliners with a new data and analytics partnership formed with IBM.

“We have launched a new program, ‘Actionable Intelligence,’ which takes our 20 plus years of experience in data collection and analytics and combines it with the power of new tools such as IBM Watson to provide solutions, rather than a reporting focus on where problems occurred,” Tempany said.

Executive and strategic policy changes were a common theme at some of the industry’s largest suppliers as well. General Electric reduced its GE Aviation division by 25 percent, or 5,400 total jobs. While commercial aviation is still the top source of revenue for GE’s aerospace division, company also saw its military segment increase to 26 percent of that total revenue in the second quarter.

During the quarter, John Slattery, former leader of Embraer’s commercial aviation division, was announced as taking over the position of president and CEO of GE Aviation for David Joyce, who retired after 40 years with the company.

An analyst asked General Electric CEO Larry Culp, during the firm’s second quarter earnings call, how the company’s commercial business will survive the downturn. His response was similar to the outlook most aerospace industry executives have at the midway point in 2020: uncertainty.

“These are difficult times in commercial aviation, but we'll work through that, all the while doing what we can to continue to feed a strong and growing military aviation within our company,” Culp said. “I don't think we have a different posture than anyone else in the industry.”