Timing is Everything: When Will IFC Consolidation Take Off?

The In-flight connectivity industry is at a crucial commercial crossroads as consolidation pressure increases on the growing number of companies vying for an ever-shrinking opportunity space.

The first flashes of promise for truly connected air travel emerged in 2004 with Boeing’s visionary Connexion in-flight connectivity (IFC) service — before being snuffed out less than two years later. Like many great ideas involving cutting-edge consumer and business technologies, it was simply too far ahead of its time. Today the entire IFC industry is at a similarly crucial commercial crossroads as consolidation pressure increases on the companies that filled in behind Connexion’s wake.

Connexion launched three years before Apple iPhone’s debut in 2007, a now seemingly ancient era when heavy laptops were the connected traveler’s tool of choice. At that time, IFC technology still had to mature: peak data rates were only 20 mbps per plane and it took three weeks to retrofit an aircraft. However, within five years after the exit, new entrants Gogo, Onair, Row-44 (Global Eagle) and Panasonic offered IFC services. Now add Viasat, Thales and Inmarsat to the mix and you have seven companies linking passengers around the world. The list seems to grow longer every day, pushing the industry closer to a tipping point.

Connecting Passengers, Chasing Profits

Ask a plane full of fliers to raise their hands if they’re not carrying a smartphone or tablet, and expect only a row or two to confess their lack of connectivity. Almost 90% of passengers have one, if not two or more devices. Moreover, the cost for airlines to connect travelers is down dramatically — less than a quarter of the $500,000 cost to outfit an airplane during the Connexion era. But despite falling costs and robust IFC demand, profitability for service providers remains elusive. Even Gogo, one of the larger providers whose stock has fared well of late, is not forecasting profitability until 2019.

The IFC strategic conundrum is not unfamiliar in service industries. Multiple providers can profitably coexist when they stick to their territory, which amounts to only a few firms competing in any given region. The difficulty occurs when firms all attempt to organically scale globally, undercutting each other in the hopes of locking up long-term business (see the rideshare industry). And as part of the process, they lock themselves into unsustainable prices. Paradoxically, part of the IFC problem can be attributed to the glut of global satellite capacity coming online. Lower bandwidth costs and a land-grab mentality are producing irrational pricing behavior. And over the past few years, candid executives from IFC service providers have acknowledged that “no one is making money” and that consolidation may be the only path to profitability.

Picking the Right Moment and Reasons for Consolidation

At this point in the IFC industry’s growth trajectory, consolidation indeed represents a canny strategy — perhaps the only sustainable one. It would enable greater bargaining power with suppliers and provide operating and marketing efficiencies from scale, all while garnering greater revenues from reduced competition.

But surprisingly, there has been no consolidation. Quite to the contrary, a plethora of new firms have tried to enter the market including Aeronet Global, Brastrading and SmartSky Networks, to name a few.

Why then are more firms entering a market that should, by all rights, be seeing a series of deals to reduce the number of competitors?

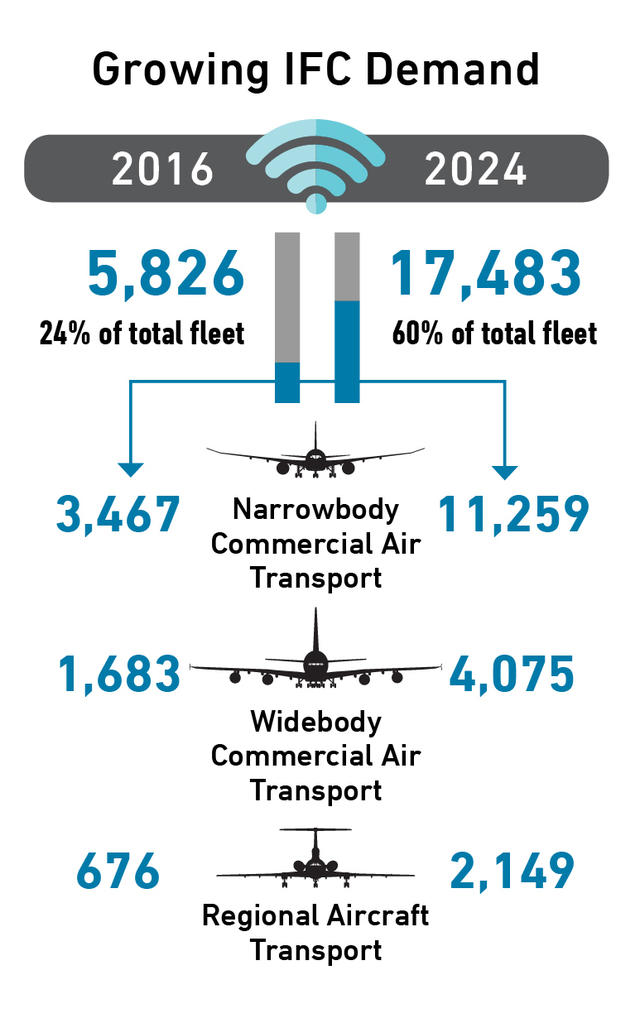

There are myriad reasons consolidation among IFC companies has yet to occur until now. The core driver behind many new ventures is uncommitted customers, and IFC seemingly has a lot of them — more than 75% of aircraft remain unconnected. And the technology used by travelers and airlines keeps evolving to require more bandwidth, be it for streaming entertainment, engine monitoring, digital retail, or crew and cabin apps.

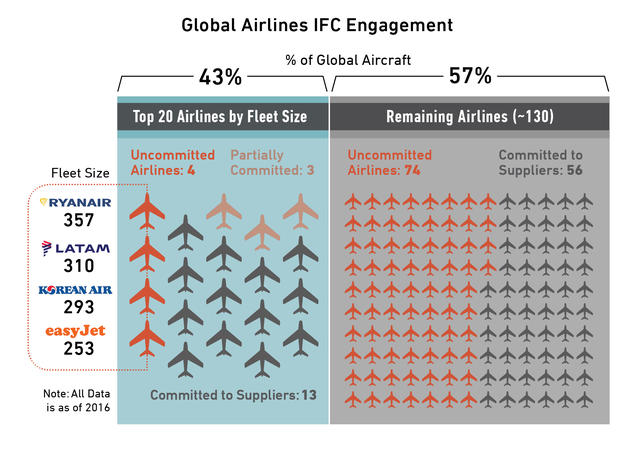

Yet consider that all but four of the top 20 global airlines have committed to or engaged with an IFC provider, and three of those four are expected to announce IFC contracts within the next 12 to 18 months. Once those remaining large airlines commit, IFC companies will have no choice but to unseat entrenched incumbents — a costly proposition — or move increasingly down the airline food chain. Such a strategy at this end of the market will yield only smaller returns. In turn, these IFC companies will find it more difficult to raise capital and support existing operations — heightening the need for consolidation.

What started off as an industry of one and a world of possibility has evolved into excessive competition and an ever-shrinking opportunity space. The land-grab is over. And now one thing is certain. Whenever the first deal is announced, more transactions will be quick to follow. It will prove, as did Connexion’s precocious debut more than a decade ago, that timing is indeed everything in the IFC sector.

The lone remaining question is: who makes the first move?